“How will bond closed-end funds do when interest rates go up?” is a popular question we’ve been fielding these days, with the Fed publicly announcing that it will likely begin increasing the Fed Funds rate starting in March. Conventional wisdom says that rising rates are bad for bonds, as bond prices generally fall when interest rates rise (and vice versa).

But does this inverse relationship also hold true for bond closed-end funds (CEFs)? Our research on historical interest rate movements and their subsequent impact on bond CEF returns may surprise you.

The Quick Answer

Contrary to what most investors may assume, our research suggests that taxable bond CEFs were an excellent fixed income investment during the most recent period in which the Fed raised interest rates (11/30/15 to 1/31/19). While the average taxable bond CEF discount widened significantly on the news and rumors leading up to the initial rate hike, the average taxable bond CEF performed well in the period following the initial rate hike and during subsequent rate hikes.

Today, municipal bond CEFs are the group that has experienced significant discount widening on news of anticipated rate hikes, and we believe they may be positioned well as we head into a period where rate hikes might occur over an extended amount of time.

The Long Answer

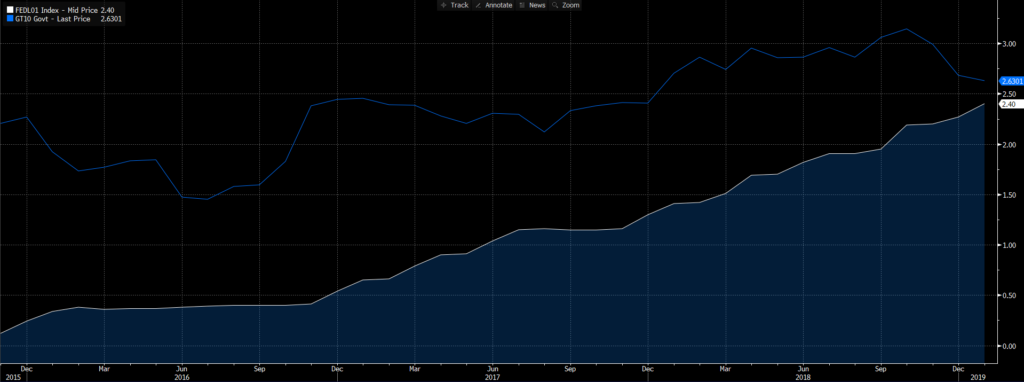

We recently took a close examination of the last time the Fed raised rates – from November 30th, 2015 to January 31st, 2019; a period where the Fed Funds rate rose from 0.12% to 2.40%. What we found was somewhat surprising:

Short-term rates rose, but longer-term rates did not rise very much. The 10-year Treasury yield went from 2.21% to 2.63% during this same period.

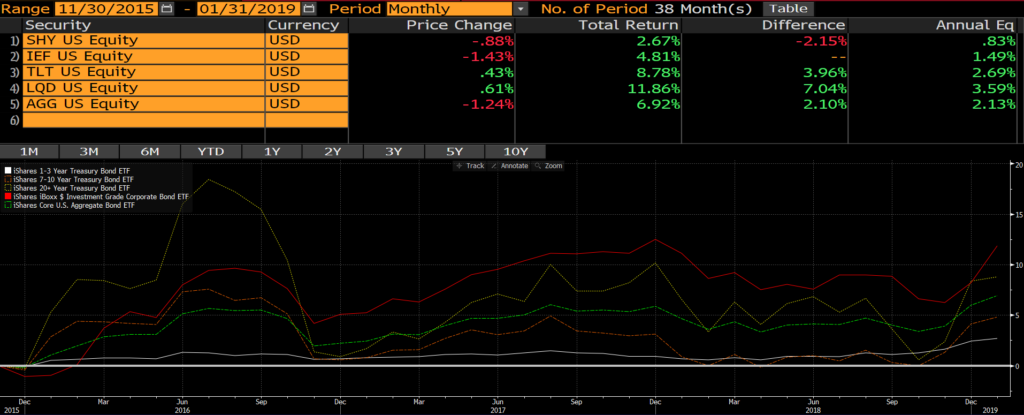

Bonds underperformed, but bond investors did not do too badly (in our opinion). Treasuries (SHY, IEF, TLT), corporates (LQD), and the overall bond universe (AGG) all returned between 1% and 4% per year over this period.

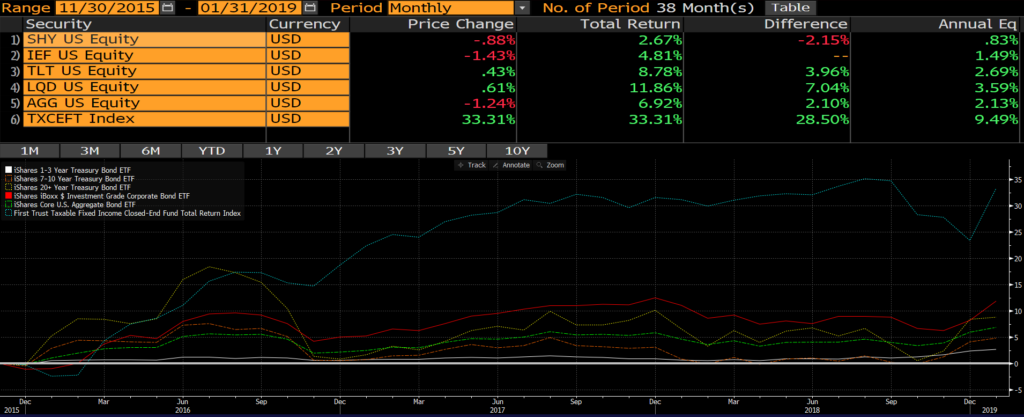

Taxable bond CEFs did even better over this period, on average. The FT Taxable Fixed Income CEF Total Return Index (TXCEFT) returned 9.5% per year (33% total return) over this period.

Why did taxable bond CEFs outperform treasuries, corporates, and the overall bond universe during this period? The answer is not that complicated: discount narrowing was a tailwind to taxable bond CEF returns during this period. Taxable bond CEFs began this period highly discounted (about 10.0% discounted on average), as retail investors had been dumping them in late 2015 in anticipation of the Fed’s action. We believe negative investor sentiment was already priced in by the time the Fed began raising rates. From that point forward, the average taxable bond CEF would ultimately narrow to about a 5.5% discount on average over the next 38 months, helping drive positive returns. Of course, it wasn’t always a smooth and constant narrowing – TXCEFT’s largest drawdown during the period was 9% (which occurred from 8/31/18 to 12/31/18), as discounts widened from 4% to 9%.

Back to current day and looking ahead, the Fed has announced that it will likely begin increasing the Fed Funds rate in March. If the Fed raises rates in a similar manner again (incrementally over an extended period), can we learn anything from the last rate hike cycle?

- Today, the 10-year Treasury yield is beginning from a similar level as in late 2015 (around 2%), and the Fed Funds rate is close to zero.

- Today, it is municipal bond CEFs which are unusually discounted, providing (in our view) a similar opportunity to what we saw with taxable bond CEFs in late 2015.

The average municipal bond CEF trades at more than a 6% discount to its NAV today, as investor angst about potential rate increases has caused significant discount widening in municipals. This group of CEFs is approximately one standard deviation more discounted than normal. While we can’t predict the future, in our view this may be an excellent opportunity to invest into municipal bond CEFs.

However, even sophisticated CEF investors may still be hesitant about whether now is a good time to invest. After all, it’s true that CEF discounts were much higher in mid-March 2020 than they are today. Wouldn’t it be prudent to wait until discounts get back to similar levels?

Our analysis of historical pullbacks in bond CEFs suggests that waiting is not necessary, and that today’s current opportunity may be too good to pass up.

Here is the data that supports this conclusion:

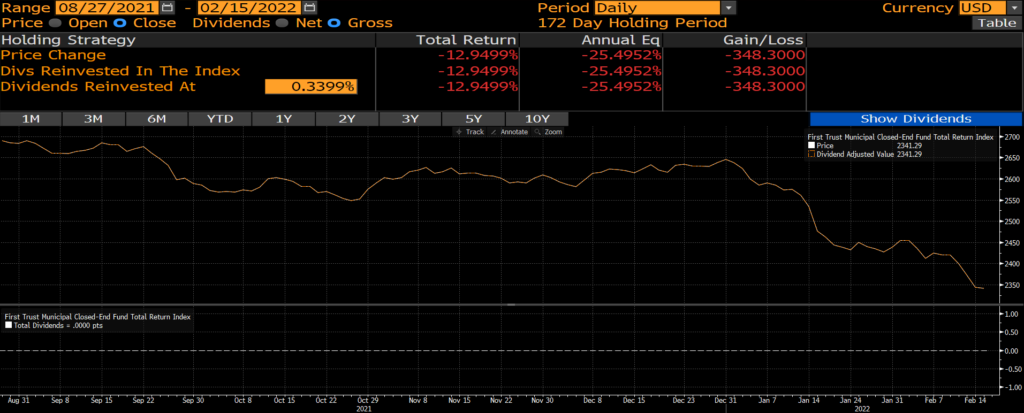

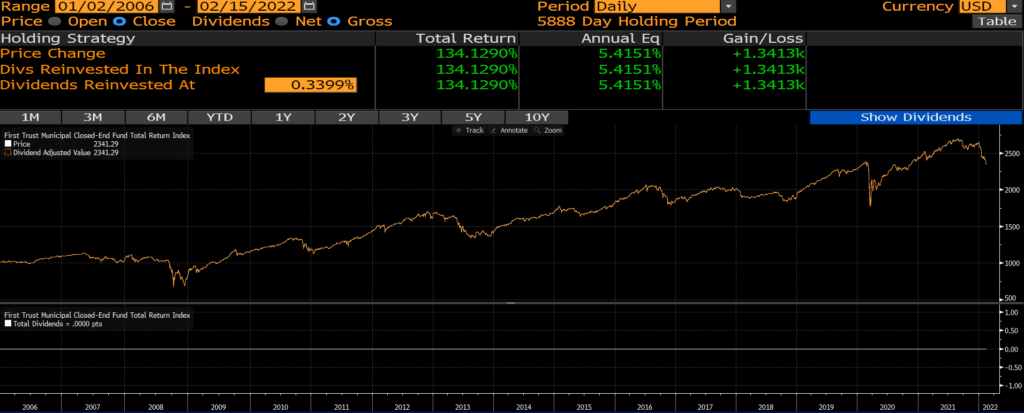

From their high in August 2021, municipal bond CEFs (the FT Municipal CEF Total Return Index (MNCEFT)) have already declined 13% (as of 2/15/22).

Examining all 27 month-ends where this index sat at least 10% below its most recent high since its 2005 inception, we find that:

- The index was 6.19% higher on average after 3 months (with 89% of those occurrences positive).

- The index was 11.53% higher on average after 6 months (with 96% of those occurrences positive).

- The index was 21.67% higher on average after 12 months (with 96% of those occurrences positive).

Out of those 27 month-ends indicated above, 18 of them were instances where Muni CEF discounts were wider than 5% on average. Measured from those 18 month-ends:

- The index was 6.55% higher on average after 3 months (with 89% of those occurrences positive).

- The index was 13.36% higher on average after 6 months (with 100% of those occurrences positive).

- The index was 23.83% higher on average after 12 months (with 100% of those occurrences positive).

In summary, we believe bond closed-end funds (and more specifically, highly discounted ones) may be an excellent option for fixed income investors to consider as they weigh their defensive options against an interest rate hike.

Disclosures and Definitions

The opinions expressed herein are those of Matisse Capital and may not actually come to pass. This information is believed to be current as of the date of this material and is subject to change at any time, based on market and other conditions. Although taken from reliable sources, Matisse Capital cannot guarantee the accuracy of the information received from third parties. Forward-looking information is based on numerous assumptions, is speculative in nature and may vary significantly from actual results based upon market conditions. This information does not constitute a solicitation nor an offer to buy or sell any securities.

An index is an unmanaged portfolio of specific securities, the performance of which is often used as a benchmark in judging the relative performance of certain asset classes. Investors cannot invest directly in an index. An index does not charge management fees or brokerage expenses, and no such fees or expenses were deducted from the performance shown.

iShares 1-3 Year Treasury Bond ETF (SHY): seeks to track the investment results of an index composed of U.S. Treasury bonds with remaining maturities between one and three years.

iShares 7-10 Year Treasury Bond ETF (IEF): seeks to track the investment results of an index composed of U.S. Treasury bonds with remaining maturities between seven and ten years.

iShares 20+ Year Treasury Bond ETF (TLT): seeks to track the investment results of an index composed of U.S. Treasury bonds with remaining maturities greater than twenty years.

iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD): seeks to track the investment results of an index composed of U.S. dollar-denominated, investment grade corporate bonds.

iShares Core U.S. Aggregate Bond ETF (AGG): seeks to track the investment results of an index composed of the total U.S. investment-grade bond market.

FT Taxable Fixed Income CEF Total Return Index (TXCEFT): a capitalization weighted index designed to provide a broad representation of the taxable fixed income closed-end fund universe. The taxable fixed income closed-end fund market is comprised of the following sectors; high yield corporate, senior loan, global income, emerging market income, multi-sector, government, convertible, and mortgage funds.

FT Municipal CEF Total Return Index (MNCEFT): a capitalization weighted index designed to provide a broad representation of the U.S. municipal closed-end fund universe.